The Basic Principles Of Chapter 13 Bankruptcy Lawyer Tulsa

The Basic Principles Of Chapter 13 Bankruptcy Lawyer Tulsa

Blog Article

An Unbiased View of Tulsa Bankruptcy Attorney

Table of ContentsSome Of Top-rated Bankruptcy Attorney Tulsa OkEverything about Best Bankruptcy Attorney TulsaOur Bankruptcy Attorney Near Me Tulsa Diaries3 Simple Techniques For Which Type Of Bankruptcy Should You FileThe 4-Minute Rule for Bankruptcy Lawyer Tulsa

The statistics for the other major type, Chapter 13, are even worse for pro se filers. Suffice it to say, talk with a legal representative or 2 near you who's experienced with bankruptcy legislation.Lots of attorneys likewise offer free consultations or email Q&A s. Take benefit of that. Ask them if bankruptcy is indeed the best choice for your scenario and whether they believe you'll certify.

Ads by Cash. We may be compensated if you click this ad. Ad Since you have actually determined bankruptcy is undoubtedly the right strategy and you ideally removed it with a lawyer you'll need to get going on the documents. Before you study all the main personal bankruptcy forms, you ought to get your own documents in order.

The Only Guide for Tulsa Ok Bankruptcy Attorney

Later down the line, you'll really require to verify that by revealing all type of details regarding your economic events. Right here's a fundamental listing of what you'll require on the roadway ahead: Identifying files like your vehicle driver's permit and Social Security card Income tax return (as much as the previous 4 years) Evidence of revenue (pay stubs, W-2s, independent profits, revenue from assets in addition to any kind of income from government benefits) Financial institution statements and/or retirement account declarations Evidence of worth of your possessions, such as lorry and realty appraisal.

You'll desire to comprehend what kind of financial debt you're trying to resolve.

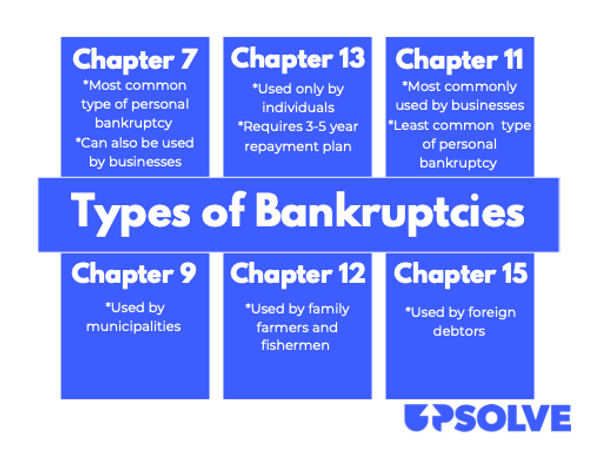

You'll desire to comprehend what kind of financial debt you're trying to resolve.If your income is expensive, you have another alternative: Chapter 13. This option takes longer to fix your debts since it needs a long-term repayment plan normally three to 5 years before several of your continuing to be financial debts are wiped away. The filing procedure is likewise a great deal more complicated than Phase 7.

The Only Guide to Which Type Of Bankruptcy Should You File

A Phase 7 bankruptcy remains on your credit record for one decade, whereas a Phase 13 personal bankruptcy diminishes after seven. Both have lasting influence on your credit history, and any type of new financial obligation you get will likely come with greater rate of interest. Before you submit your insolvency types, you must first complete a required course from a debt counseling agency that has been approved by the Division of Justice (with the remarkable exception of filers in Alabama or North Carolina).

The training course can be finished online, in individual or over the phone. You must finish the training course within 180 days of declaring for insolvency.

Tulsa Debt Relief Attorney Things To Know Before You Get This

Examine that you're submitting with the proper one based on where you live. If your long-term home has actually moved within 180 days of filling, you must submit in the area where you lived the better part of that 180-day period.

Commonly, your personal bankruptcy lawyer will work with the trustee, however you may need to send the individual records such as pay stubs, tax returns, and savings account and bank card declarations straight. The trustee who was simply appointed to your instance will certainly quickly establish a mandatory conference with you, referred to as the "341 conference" due to the fact that it's a requirement of Area 341 of the united state

You will certainly need to offer a timely list of what certifies as an exemption. Exceptions might put on non-luxury, key cars; essential home products; and home equity (though these exceptions policies can vary widely by state). Any type of home outside the checklist of exemptions is considered nonexempt, and if you do not provide any type of listing, after that all your building is taken into consideration nonexempt, i.e.

You will certainly need to offer a timely list of what certifies as an exemption. Exceptions might put on non-luxury, key cars; essential home products; and home equity (though these exceptions policies can vary widely by state). Any type of home outside the checklist of exemptions is considered nonexempt, and if you do not provide any type of listing, after that all your building is taken into consideration nonexempt, i.e.The trustee wouldn't market your sports automobile to quickly repay the financial institution. Instead, you would certainly pay your financial institutions that amount over the training course of your settlement strategy. A typical misunderstanding with bankruptcy is that when you submit, you can quit paying your debts. While bankruptcy can help you eliminate numerous of your unprotected financial debts, such as past due medical costs or individual car loans, you'll intend to maintain paying your monthly payments for secured financial debts if you intend to keep the residential property.

Getting My Tulsa Debt Relief Attorney To Work

If you go to danger of foreclosure and have tired all various other financial-relief options, then filing for Phase 13 may postpone go to this site the repossession and assist in saving your home. Inevitably, you will still require the earnings to proceed making future home loan repayments, as well as paying off any type of late settlements over the program of your settlement strategy.

The audit might delay any type of debt relief by a number of weeks. That you made it this far in the procedure is a respectable sign at least some of your debts are eligible navigate to this web-site for discharge.

Report this page